U.S. apparel sourcing trends: A shift in momentum amid economic uncertainty

Share This

A review of the most recent data from the U.S. Department of Commerce’s Office of Textiles and Apparel (OTEXA) reveals significant shifts in U.S. apparel sourcing behavior as of early 2025. These shifts highlight both the cautious mindset of fashion companies and growing global challenges in the apparel supply chain.

Slowing growth in apparel imports

After a sharp increase in late 2024 and January 2025, U.S. apparel import growth has now started to level off. In February 2025, import value rose by just 3.2%, and volume by only 1.5%. This modest uptick contrasts sharply with the 18–19% gains seen a few months earlier. It suggests that much of the earlier surge was likely driven by concerns over anticipated tariff hikes, rather than a true rise in end-consumer demand.

Adding to this cautious sentiment, American consumer confidence has dropped sharply. The Consumer Confidence Index sank to 92.9 in March 2025—its lowest point in two years. Even more concerning, the Expectations Index fell to 65.2, the weakest since 2013. With economic uncertainty looming and potential reciprocal tariffs ahead, many U.S. fashion brands could begin cutting or postponing sourcing orders.

Apparel import costs continue to climb

Price pressures are becoming more evident across the apparel trade. During January and February 2025, the average cost per square meter equivalent (SME) for imported apparel rose to $3.06, a 1.3% increase over the same period last year. Leading suppliers all experienced notable price hikes: China +2.9%, Vietnam +3.6%, Bangladesh +2.6%, Mexico +4.7% and CAFTA-DR +0.6%.

These cost increases reflect rising expenses across labor, raw materials, and logistics. If new tariffs are implemented under the Trump administration's proposed policy changes, prices may escalate even further—adding more strain to sourcing budgets.

Regional dependence persists despite calls for diversification

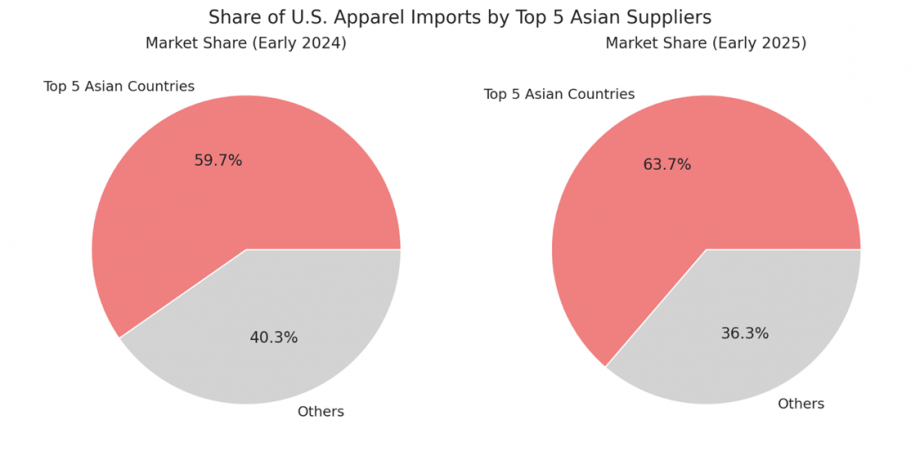

Despite ongoing discussions about diversifying sourcing strategies, U.S. fashion companies have made minimal changes in their sourcing geography. In February 2025, Asian suppliers still accounted for 71.5% of the total import value—unchanged from the previous year. Moreover, the top five apparel exporters to the U.S. (China, Vietnam, Bangladesh, Cambodia, and India) increased their collective share to 63.7%, up from 59.7% in early 2024.

Even China’s position appears stable, with an 18.4% share in value and 32% in volume—roughly the same as last year. These figures suggest that brands are hesitant to restructure their supply chains significantly, especially when tariffs now apply across nearly all sourcing destinations. Traditional diversification strategies may no longer provide the risk mitigation they once did.

Interestingly, the United Nations Comtrade database indicates varied dependency on the U.S. among Asian exporters. While Vietnam, Sri Lanka, and ASEAN nations send roughly 40% of their apparel to the U.S., China and Bangladesh rely far less—only around 20% of their exports go to the American market. In contrast, countries like Mexico and CAFTA-DR members remain highly dependent on the U.S. due to regional trade partnerships and supply chain integration.

Nearshoring yet to gain ground

Contrary to industry hopes, there’s little evidence of a shift toward nearshoring in the Western Hemisphere. In February 2025, CAFTA-DR countries supplied only 7.6% of total U.S. apparel imports by quantity, down from 9.6% a year earlier. Mexico’s share also declined slightly to 2.3%, compared to 2.4% the year before.

However, there are some bright spots. The CAFTA-DR preference utilization rate climbed to 81.1% (January–February 2025), up from 73.8% a year earlier. Additionally, more than 75% of apparel imports from this region now meet the “yarn-forward” rules of origin, indicating improved compliance with trade agreement requirements. Still, use of the “short supply” rule remains minimal—just 2% so far in 2025.

Conclusion

As the U.S. apparel industry braces for economic headwinds, fashion companies are navigating a delicate balance between cost, reliability, and trade policy risk. Slowing imports, rising prices, and a lack of meaningful sourcing shifts suggest that the road ahead will require more strategic decision-making than ever before.